Let’s start with some basic facts everyone knows about Social Security:

- After you reach retirement age, everyone in the US starts Social Security payments for the rest of their life.

- If you strike it rich and retire early, Social Security will be there waiting for you decades later.

- Social Security taxes are high enough, but at least you don’t have to pay tax on your Social Security income in retirement.

This is all great news, but there’s one little problem.

EVERYTHING I JUST SAID IS TOTALLY FALSE.

That’s right, these are myths. Now let’s look at what is ACTUALLY true.

The Backstory

In 1935, FDR signed into law The Social Security Act. The purpose: to help pay retirees that were 65 or older. The system: You earn credit for every year you work. Your monthly retirement benefits are based on the money you made and how many years you’ve been in the workforce. The Social Security Administration (SSA) then uses a lot of math and formulas to calculate your monthly benefits. If all you want to know is how much money you’re supposed to get, that’s easy to find out. Just create an account on SSA.gov and they’ll tell you.

Here’s What They Don’t Tell You:

- What exactly are Social Security Credits?

- How many years do I have to work to make bank?

- How long do I have to wait before I can start getting benefits?

- How do spousal benefits work?

What Exactly are Social Security Credits?

Social security credits are like a trigger. Have enough and you earn benefits. Don’t have enough and, tough luck, you get nothing or next to nothing.

To qualify for social security benefits, you must earn at least 40 social security credits during your working years. 39 won’t cut it. Plus, the number of credits is like a door-opener, but it has nothing to do with how much money you will get. It’s simply about whether you’re in the system or out of it.

But, wait, there’s more. You’d think if you had a banner year, you’d get tons of credits. But NOOOO. In fact, the only thing you probably have in common with Bill Gates is that you both earn the same number of credits each year: four. Because four is the maximum. And that means you’ve got to work at least 10 years—or more, if any year you don’t even make your 4 credits. Once you’re 62, if you don’t have 40 credits, you’re busted out. No Social Security for you—ever! But if you have at least 40 credits by age 62, welcome to the club—you’re in.

OK, so how do you earn these credits?

Simple: by paying into social security. And there are two ways to do this:

- By working for somebody as their employee (W-2 wages), or

- By being Self-Employed (as an independent contractor) and paying self-employment tax

But wait, “Can I buy social security credits?” No. You can’t buy them, transfer them, or borrow them. You must earn them.

There is a minimum amount of money you must earn each year to get a social security credit. And every year that amount changes because of inflation. Inflation, now there’s a word you may have heard of recently. For instance, in 2022, you earn one social security credit by making at least $6,040. That means if you make four times that or $24,160 this year, you will get the bonanza of four Social Security Credits. Yep, just like Bill Gates. You could make one trillion dollars and you’d still only get those measly four credits. Life is tough.

But once you hit the big 40, you are now eligible to collect social security, provided you’re old enough or disabled enough.

You can look up how many social security credits you have on SSA.gov.

How many years do I have to work to get Social Security?

Ten years, minimum, as explained above. But remember, the SSA calculates your monthly benefit based on how much money you made, not based on the number of credits you have. The SSA first looks at all the years you’ve worked. Then they take the 35 highest paid years (indexing for inflation the amounts you made) and use the average of those years to calculate your benefit.

If you don’t have 35 working years, they will add zeroes for the remaining years when you didn’t work. In other words, if you only worked 30 years, they would add five years of zeroes. You don’t want zeroes since it will lower your monthly benefits when they calculate your average.

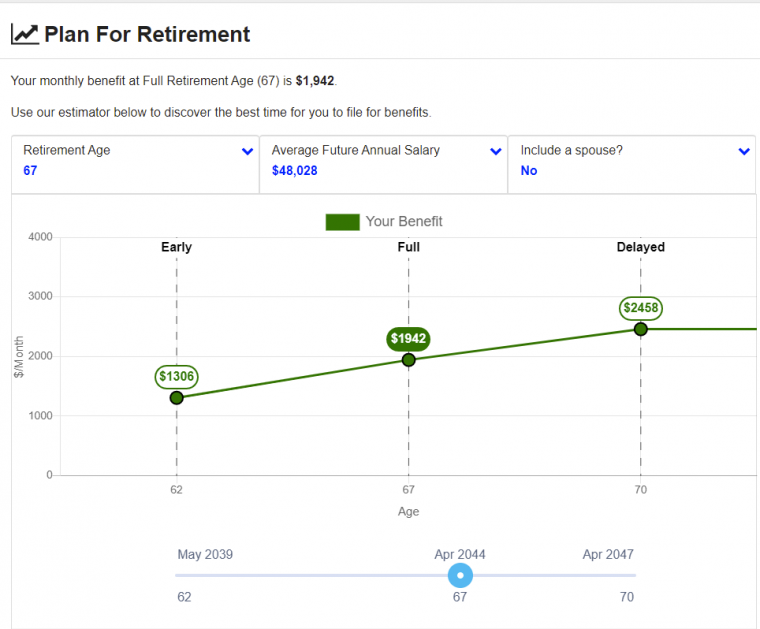

When can I start taking benefits?

You can start taking social security benefits as early as at age 62, but of course there’s a catch. The earlier you start, the lower your monthly benefits. The longer you wait, the higher your monthly benefits. In other words, the SSA uses a carrot and stick. Here is a breakdown:

- Early (age 62, but before age 67)

- Full (at age 67)

- Delayed (after age 67, but before age 70)

As you can see from the chart, the longer you wait the more you get per month, so long as you stay alive. If you decide to take your benefit early, they will pay you less every month. That’s because you will get extra months of payments.

How do spousal benefits work?

What if you didn’t work enough to qualify for Social Security? Good news. If you are married and your spouse qualifies with the magical 40 points, you can still get Spousal Benefits even if you have fewer than 40.

To quality for these spousal benefits:

- You must have been married for at least 1 year

- Your partner must have already applied for their benefits

- You must be at least 62

Then, you will be entitled up to 50% of their benefits.

Example:

Steve and Betty are married. Steve worked enough to be eligible for Social Security, but Betty didn’t. When Steve is ready for take his full retirement benefits at age 70, he is entitled to $2,000 a month. Since Betty is 62 and married to Steve, her spousal benefit is $1,000 (50% of Steve’s $2,000). But Steve still gets his $2,000, so, together, Betty and Steve are getting a benefit of $3,000.

But what if you are in a domestic partnership but not married? Well then you are SOL my friend. The US government only recognizes marriages. If you’ve been living together in non-marital bliss for 50 years, you are nothing to the SSA and nothing is what you shall get from them.

Now let’s cover some general questions.

Should I take benefits early or later?

Here’s a list of pros and cons of taking benefits early:

Pros

- Spousal benefits get unlocked

- You’ll have the extra cash early to spend early in retirement

- You get the money earlier if you need it

- You’re in poor health and are afraid you won’t be able to collect later

Cons

- Your benefits will be reduced, permanently

- Your COLA (cost of living adjustment – inflation adjustment) will be lower

- If you keep working, your social security will be reduced until you are 67

Everybody’s personal situation is different. I recommend checking with a financial planner to see what’s best for you.

Are social security benefits taxed?

They never used to be but Congress “fixed” that. As you know when Congress fixes something, it means that you pay more taxes no matter what. Still, there is a limitation on this. You get taxed only if you are making money while collecting social security benefits. If the only money you make is social security, it’s not taxed. Up to 85% of your benefits may be taxed and it’s based on IRS minimum income totals.

In 2022, your social security will be taxed, if you’re:

- Single making over $25,000,

- Married making over $32,000, combined

Conclusion

Like any system, Social Security has a morass of rules and regulations. Ignore them only at your financial peril. Know them and use them to your advantage so you end up with more money coming in and less taxes going out. After reading this article, you should be in the second camp.

Also, if you enjoyed this article consider checking out our articles below on NFTs, Capital Gains, and IRAs.