In today’s job market, companies are having a hard time hiring talent. When a prospect walks through the door, the expectation has become, “Show me the money!” Common ways companies show employees “the money” is through employee benefits such as: 401(k) retirement matching, family health insurance, on-site child day care, remote work, and company stock and stock options.

Company stock sounds exciting, but if you’ve never been offered it before, it’s confusing. Let’s be honest, most people have no idea how it works. You’re just hoping your company either gets acquired, or goes public, so you get paid out. But guess what? If your company is successful and your stocks are worth a boatload of money, Uncle Sam is waiting to get his cut. We are going to show you what taxes to expect for both employee stocks and stock options.

The Most Common Stock Incentives

There are too many stock incentives for us to cover them all. We’re going to cover the most common ones:

- RSUs – Restricted Stock Units

- NSOs – Non-Qualified Stock Options

- ISOs – Incentive Stock Options

Stock Lingo

First things first: before we get into all the different types of stocks, options, and their tax consequences, there are a lot of terms and lingo you may not be familiar with. I want to make sure you know the important ones, so we’re going to go over them:

| Term | Definition |

|---|---|

| Stock Option | The right to purchase company stock at a specific price |

| Grant Date | The date that the company gives you the right to acquire stocks or options |

| Exercise Price | Specific price you are allowed to purchase the stock for. Also referred to as the Strike Price |

| Expiration Date | The last date you are allowed to exercise your stock option |

| Vesting Period | Amount of time you must wait before you’ve earned your stock or option |

| Vesting Requirement | Vesting based on a certain outcome or achievement |

| Cliff | The minimum amount to time you must wait before any vesting begins |

Here’s an example using stock lingo:

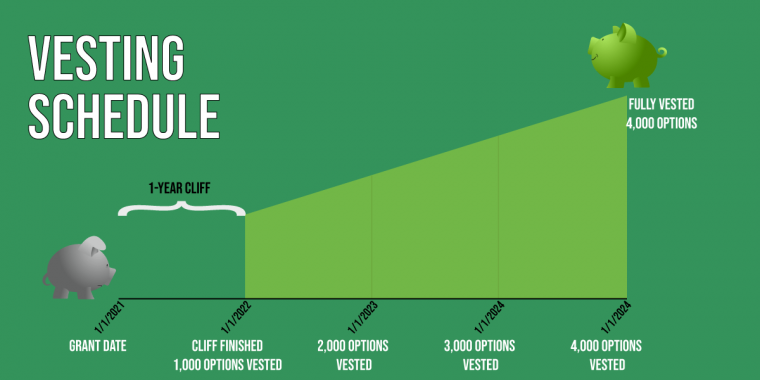

Steve starts working at ABC Inc. on January 1st, 2021. When hired he’s offered 4,000 stock options at $1.13 per share. However, there is a 4-year vesting period, with a 1-year cliff.

Since his vesting period is 4-years, and there are 48 months in four years, he will vest 83.333 shares every month he works at ABC Inc. However, because of the 1-year cliff, Steve won’t receive any stock options until he’s worked at ABC Inc. at least a year. After 1 year he will have vested 25% of the shares (1,000 options). He will vest another 83.333 shares every month he continues working for ABC Inc. for the remainder of the vesting period. Here’s a visualization:

In other words, if Steve quits or gets fired before 1 year of employment, he gets nothing. But once he’s worked there for at least a year, 25% of his stock options vest.

RSUs – Restricted Stock Units

RSUs are usually offered by large companies such as Google, Facebook, Amazon, etc. They can be issued to both employees and independent contractors (non-employees). Unlike stock options, RSUs do not have to be purchased by the recipient. They have a grant date and are usually subject to vesting. Once they’ve become vested, RSUs are taxed as ordinary income (the worst tax rate).

Your thinking, “What about capital gains tax?” If you want to pay less tax when you sell your stocks (i.e., capital gains), you must hold the stocks for 1 year or more after the RSUs have vested. In other words, after you’ve already given the IRS money.

RSU example:

Kyle in an independent contractor that does patent work for ABC Inc. As part of his compensation, they’ve offered him RSUs, with a vesting period of 2 years and vesting requirement that he applies for and is awarded patent from of the USPTO. At the end of 2 years, he is successfully awarded the patent, and the stocks became fully vested.

Kyle is in a 30% tax bracket. When he fully vests, the stock’s Fair Market Value (FMV) is $25,000. He must now pay the IRS $7,500. A little over 1 year later he sells the stock for $57,500. He now pays capital gains tax (15%) on the spread between when he received the stock and when he sold it (remember, he already paid tax on the first $25,000, so he doesn’t pay tax on that again). Here’s the math:

- Ordinary Income Tax (30%) – $25,000 x 30% = $7,500

- Capital Gains Tax (15%) – $32,500 ($57,500 – $25,000) x 15% = $4,875

In total Kyle paid $12,375 in taxes. He paid less tax when he sold the stock, because he held it over a year. If he had sold it before 1 year, he would’ve paid ordinary income tax of $9,750 ($32,500 x 30%) instead of capital gains tax of $4,875.

Difference between Restricted Stock and RSUs

It’s important that we take a moment and explain the difference between Restricted Stock and Restrictive Stock Units, since they are often conflated.

Restricted Stock is stock that is earned by somebody working for a company, usually subject to some form of vesting before they are earned. They are normally granted upon being hired, but if certain conditions aren’t meet, the restricted stock may be forfeited or bought back by the company.

On the other hand, Restricted Stock Units is a promise that a company will grant you stock at a future date. This means you have no voting rights until the stocks are granted. Another difference between Restricted Stock and RSUs are tax consequences. For instance, you are allowed to make an 83(b) Election with Restricted Stock, but not RSUs.

What’s an 83(b) Election that I’ve heard about?

If you follow financial gurus, you’ve probably heard that Warren Buffett pays tax at a lower rate than his secretary. That’s because he does everything legally possible to pay long-term capital gains while avoiding ordinary income tax. To be like Warren Buffett, you need to make more money with long term capital gains. The 83(b) election helps you do exactly that.

If you’re granted restricted stock, the IRS lets you make a special election to help you pay more long-term capital gains and less ordinary income tax. You do that by filing a section 83(b) election with the IRS. You will now pay ordinary tax on the FMV of your restricted stock when it is granted, instead of when they are vested.

Kyle paid ordinary income tax on $25,000 because that was the FMV when the stock was vested. But let’s assume that Kyle was tax savvy, knew about the 83(b) election, and filed it with the IRS on time. If on the grant date the FMV of the stock was only $10,000 instead of $25,000. He would pay less tax:

- Ordinary Income Tax (30%) – $10,000 x 30% = $3,000

- Capital Gains Tax (15%) – $47,500 ($57,500 – $10,000) x 15% = $7,125

Kyle saved an extra $2,250 because he made an 83(b) election.

How do I file an 83(b) election?

Here’s what you need to know:

- You must file an election with the IRS within 30 days of the grant date (this includes weekends and holidays)

- Mail the election to the IRS address that you would normally file your tax return. Here’s a link

- Deliver a copy of the election to your company

- The election letter should state your name, address, social security number, tax year, the restricted stock, and FMV on the grant date

- Your election to the IRS should also include a second copy, with a return address envelope, to be stamped and returned to you

Still confused? Don’t worry, we will be writing an article with sample election letters and examples. We’ll link it to this page in the coming weeks.

NSOs – Non-Qualified Stock Options

NSOs, also referred to as NQSOs, are usually offered by small to mid-sized private companies or startups. Unlike RSUs, they are options so they must be purchased. That means they are riskier since you can lose money if the company goes out of business. You are taxed when you exercise your NSOs. Like RSUs they are subject to ordinary income tax, but not on vesting. Instead, their tax is based on the spread between the strike price and FMV.

Example: if you are awarded 4,000 NSOs, the FMV of the stock is $5 a share, the strike price is $1.13, your tax would be:

- Taxable Amount – 4,000 shares x $3.87 ($5 – $1.13) = $15,480

- Ordinary Income Tax – $15,480 x 30% = $4,644

Just like RSUs, if you hold the stocks for over 1 year before you sell them, the gain on the sale becomes long term capital gains, which is taxed less.

ISOs – Incentive Stock Options

ISOs are often referred to as Qualified Stock Options. They’re offered by smaller companies and startups. They are preferred to NSOs & RSUs, since the entire gain may qualify for long term capital gains. In other words, you will be more like Warren Buffett and will not have to pay ordinary income tax. However, as all things IRS, these stock options must qualify to be ISOs. Here’s the criteria:

- You must be an employee of the company (consultants, independent contractors, and non-employee board members are out of luck)

- Strike price of the option must be at least FMV of the stock when granted

- There is no deduction for the company when issuing the options

- The holder of the stock must not sell the stock for at least 1 year after exercised, and 2 years after the grant date.

- It cannot be transferable

- Must be exercisable no more than 10 years after the grant date

How can I get Long Term Capital Gains with ISOs?

There are two types of taxes you need to be aware of with ISOs. They are AMT and Long Term Capital Gains.

Alternative Minimum Tax (AMT) – is additional tax that you have to pay if the government thinks you’ve made too much money, but not paid enough tax. When you file your tax return every year, your accountant calculates both your regular tax and AMT. You pay whichever is higher. When you exercise your ISOs, the spread between the strike price and FMV is added as an increase to calculate your AMT. So, it’s possible you will have to pay AMT. However, if you pay AMT, you may receive a tax credit in future years called the Tentative Minimum Tax Credit that you can carryforward.

Long Term Capital Gains for ISOs – to qualify you must sell your stock 2 years after the grant date, and 1 year after you’ve exercised the stock. If you sell your stock too early, you will pay ordinary income tax on the gain. So, the key with ISOs is patience.

What about Qualified Small Business Stock (QSBS)?

Qualified Small Business Stock is a special type of stock that you may not have to pay any tax on at all. It’s very detailed and complicated, so we wrote an entire article about it here.

Is there more?

There is always more because the tax code is complicated. We covered the most common stock incentives, but not every possible topic. That’s why we recommend that you contact a CPA to go over the fine details of your stocks and options that you’ve been granted.