You’ve probably heard of compound interest but might not be sure how it works. You’ve been told that it’s important but may not know why. One of the smartest people that ever existed, Albert Einstein, once said “Compound interest is the eighth wonder of the world. He who understands it, earns it…he who doesn’t…pays it.”

Simply put, understanding compound interest makes your money grow quickly. That’s because you’re making money on-top-of the money you’ve already earned. All the wealthiest people I know understand compound interest.

As Einstein said, people who don’t understand it, either pay for it, or at the very least, don’t grow their wealth fast enough.

Understanding Compound Interest will help you grow your money faster. I’m going to show you the importance of understanding compound interest.

- What exactly is Compound Interest?

- How Compound Interest works

- How paying too much tax destroys your Compound Interest Growth (CIG)

- How the IRS uses Compound Interest against you

What is Compound Interest?

Compound Interest is interest that you make on both the principal you deposit and interest that has accumulated over time. That probably sounds like math gibberish to you, so simply:

Compound interest is interest you earn on Interest.

How does Compound Interest work?

Here’s an example: you have $1,000 of money to invest so you go to your bank and find out that you have the option to invest it in a CD (certificate of deposit). The bank offers pays you 6% interest for a year: the options are –

- simple interest (no compounding),

- interest compounded quarterly,

- interest compounded monthly, or

- interest compounded daily.

Here’s a chart of the differences between the options listed above.

| Compounding | Interest Actually Earned |

|---|---|

| Interest 6% – no compounding | 6% |

| Compounded Quarterly 6% | 6.13636% |

| Compounded Monthly 6% | 6.16778% |

| Compounded Daily 6% | 6.18313% |

You’re probably saying to yourself, 6% vs 6.18313% isn’t really that big of a deal, is it? You’d be wrong.

It makes a monumental difference, over your lifetime! Warren Buffett is one of the greatest investors in the world, not because his average return is 22%, but because it’s 22% compounded over his lifetime.

“My wealth has come from a combination of living in America, some lucky genes, and compound interest.” -Warren Buffett.

Even though Compound Interest doesn’t make much of a difference in 1 year, over your lifetime it can cost you millions of dollars. Here’s an example.

A King, a Chessboard, and a Loss of Fortune

There is a famous parable about compound interest and a King that loved to play chess.

The story goes, the King offered to grant a wish to anybody in his kingdom that could beat him at chess. One day, an old wise sage had beaten the king and when asked what his wish was, the sage asked that the King grant him “one grain of rice on the first square of a chessboard. Then two grains on the next square, four grains on the following, eight grains on the one after that, and so on and so forth so that each square doubles the previous square for all 64 squares of the chess board.” The king, being perplexed (and not understanding compounding) agreed to the terms.

Here’s how it played out:

By understanding compound interest, the wise sage was able to bankrupt the kingdom (by compounding his wealth every new square.)

But what happens to your compound interest growth if you get taxed first?

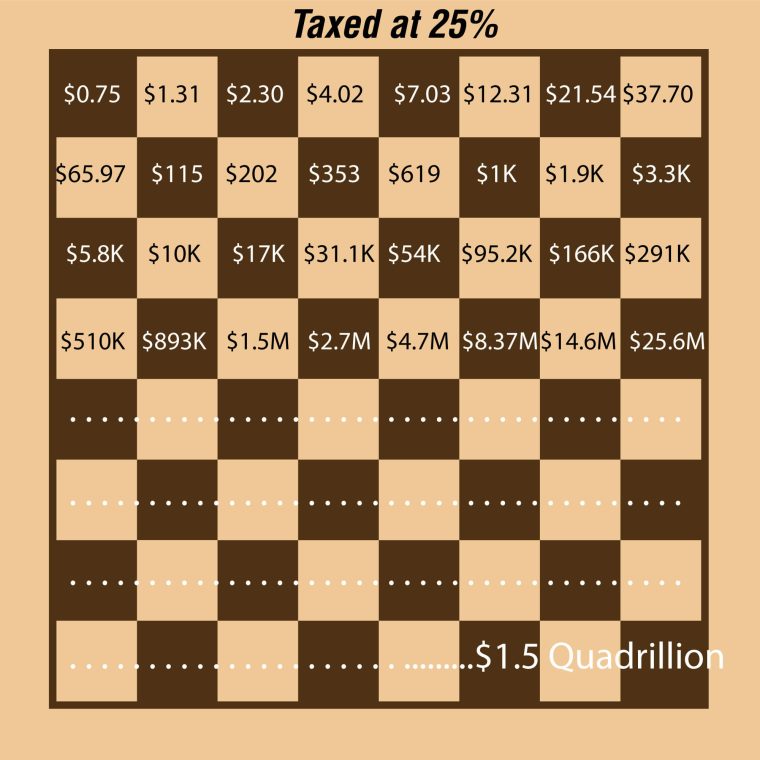

How Paying Tax Destroys Compound Interest Growth

Let’s use the same example as above, but instead of doubling your money every time you go to the next square, every new dollar you receive gets taxed 25% first.

By the time you reach the 32nd square, 25% tax reduces your earnings from $2 Billion to $25 Million (which means 98% of your potential growth went to the taxman.) This is why the wealthy try to pay the least amount of tax possible!

I know most people will not create a billion-dollar company, so the difference in this example may seem like it doesn’t apply to you.

But for the average person, not understanding compound interest will make difference between a few hundred thousand and a few million when you retire – which will make a huge difference.

How the IRS uses Compound Interest Against You

When the IRS charges you interest for paying your taxes late, they make sure to charge you highest possible interest, which is interest compounded daily. At the time of this article, the IRS’ current interest rate is 8%, in reality it’s 8.32776% because of compounding (and in Canada, they just announced that their interest penalty is 10%+.)

Don’t Get Taxed by Your Taxes

If you enjoyed this article, consider signing up for my weekly newsletter. Where you’ll receive tips like this that help you grow your wealth, keep more of your money, and pay less tax.

[contact-form-7 html_id=”newsletter-web” id=”243″ title=”Newsletter subscribe”]